6 Mistakes First Time Home Buyers Should Really Avoid

As a first time buyer, navigating the property market can be difficult – particularly if you are not aware of the process involved in purchasing a residential property. However, all hope is not lost, because with a little thought and preparation, purchasing the first home will be much less difficult and costly. Here, we’ll go over 6 common first time home buyers mistake should avoid:

Common First Time Home Buyers Mistakes Should Avoid:

#1 – Not Getting an Agreement in Principle:

Although it’s possible to get caught up in the thrill of house hunting, it’s crucial as a first time home buyers to first figure out the mortgage options. It’s a smart idea to get a Decision in principle before you start looking for property. An agreement in principle, also known as a ‘Decision in Principle’ is a certificate from the mortgage lender that shows how much you can borrow. These are valid for anywhere from 30 to 90 days. Although it isn’t an official offer from your lender, it offers you a good understanding of your budget and shows sellers and estate agents that you’re serious about buying and can afford the house. Failure to obtain a DIP may lead to disappointment, especially if you find a property you like but are unable to obtain a mortgage to buy it.

Also Read: 5% Deposit Mortgage Scheme in the UK for First Time Buyers and Homeowners

#2 – Underestimating How Long It Takes To Get a Mortgage:

Unfortunately, when it comes to securing a mortgage, there is no set deadline for the mortgage to be approved. While most home buyers would expect to wait between submitting a full application and receiving a mortgage offer which could take from 3 to 30 days, it could even take much longer. Before running into making an offer on a house, it’s important to get all the necessary documentation and DIP in place and submit the application as soon as the offer is accepted on purchased property.

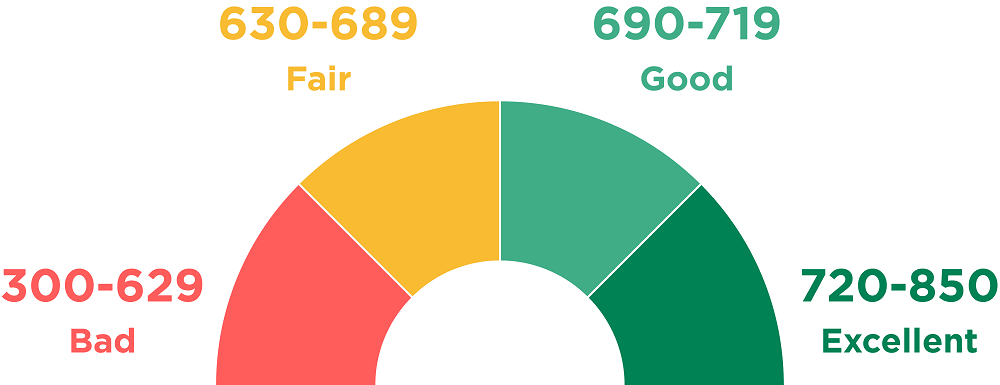

#3 – Not Checking Your Credit Score:

Your credit report is the showcase of your financial history that lenders can review before determining whether or not to lend to you. You run the risk of getting your application denied if your credit is bad. Rejected applications would be counted against you, which may hurt your credit score even more. It’s important to review your credit score before submitting so that you can fix any mistakes on your record and get your credit rating in the best possible form. And if you have a bad financial background, such as defaults or County Court Judgments (CCJs) or missed payment, you may be able to get a mortgage. Our guide to poor credit mortgages will explain to you more in detail.

Also Read: Type of Mortgages – Know Which Mortgage is Right For You

#4 – Underestimating How Much It Costs To Buy a Home:

Buying a home is one of the biggest financial decisions most people make in their lifetime. It involves few additional costs which one should be aware of before starting the process and should arrange their finances as per that. The additional cost may involve Conveyancer fee, Valuation fee or product fee also known as arrangement fee. The buyer also needs to be aware of Building and Content insurance which needs to be taken from the date of exchange of contract.

#5 – Using The Wrong Solicitor:

The overwhelming majority of mortgage lenders have a list of conveyancers who are willing to represent them. If you choose a solicitor that isn’t on their panel, they will not be willing to act on your lender’s side, which means you’ll have to pay further to have one of their licenced solicitors instructed. If you’re looking to keep expenses down, review the lender’s accepted list before choosing a conveyancer to make sure you’re not overpaying.

Also Read: How To Choose Mortgage Broker That’s Right For You – An Ultimate Guide

#6 – Doing No Research Into The Area:

It’s a smart idea to figure out your preferences for the place you’d like to move in before registering with an estate agent or beginning to search online. Whether you want good transportation, a lot of open land, good schools, or a variety of facilities such as supermarkets, restaurants, and gyms, for example? It would be easier to choose a location if you have a clear picture of what you want. If at all practicable, spend a day or two in places you like but are unfamiliar with to get a true sense of the environment and how strong the transportation connections are.

Your first-time buyer tale could be the deciding factor in the deal – just try to avoid first time home buyer mistakes.

Our knowledgeable mortgage advisors will walk you through everything from interest rates to deposit criteria, as well as what your monthly outgoings will be with a range of mortgage options.

If you’re hunting for a first-time buyer mortgage and have some doubts or concerns, Mountview Financial Service will assist you in determining the right remortgage choices. Call us at 02080950120 for more details or send us an email at info@mountviewfs.co.uk for more information.