What is Mortgage – A Beginner’s Guide?

Taking loans is all about meeting unforeseen or sudden expenses that crop-up from nowhere and disturbs the entire month’s budget. These days, the scenario is such that people are facing a lot of problems in business and many have lost their jobs. This has led to the financial crunch in everyone’s life. And here is the point where mortgages or loans come into practice as saviors of life. According to the companies providing best mortgages for first time buyers, you have to keep something or the other as collateral to get the loans sanctioned. Besides this, the one taking loan is required to pay the interest accrued on the principal amount too. Generally, the loan amount and the interest are collectively divided in equal monthly installments. So, it becomes easier for you to pay off within the decided time period. But, there are many who might not have taken out a mortgage before. For them, complete information on the mortgages, process, tenure, and eligibility is provided.

Overview of Mortgages:

A mortgage is fundamentally a borrowed sum of amount taken from a bank or financial institution for buying a property. This loan can be paid off in a decided time period while staying in the property as well. Generally, the mortgages initiate on a special rate which usually continues till five years. After the initial interest rate time is over, you have to shift over to the lender’s standard variable rate or SVR. It should be noted that this interest might be higher than the standard version. But, the best thing is that the mortgage buyer will be able to remortgage to a more special deal at this point.

It is a natural fact that anyone lending the money would like to be assured of repayment from the buyer. This brings the possibility that the lender might ask several questions as a part of their confirmation process that may include monthly income, expenses or even other loans going too. So, one should not hesitate to answer such questions in any way.

Also Read: Tracker Mortgage: Definition, Pros & Cons

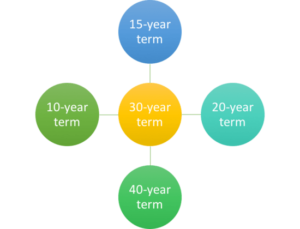

Time Period of Mortgages:

Taking note of the time period required to pay off mortgage as a part of a first time home buyer guide, the typical term lasts till 25 years. But, there are other lending companies that may extend the time period to 30 years, by considering your age and conditions. It does not mean that you will have to bear the burden of the mortgage till 25 or 30 years, you can opt for a shorter time period too. But, make sure to adhere to the rules and repay the amount within that time slot. Indeed, the buyer of a mortgage loan can opt for 5, 10, 15, or even 20 years of time to pay off loan.

One thing to be noted in this matter is that a longer time period will have lower monthly installments; but, the interest amount will increase as per the extended time period. On the other hand, the shorter mortgage term will bring higher installments and lesser interest as the loan gets closed quicker.

Types of Mortgages:

Though there are various mortgages, the most famous ones are 15-year and 30-year fixed ones. Some of the mortgage loans can be stretched over; while, other people go for a shorter time frame. The longer ones accrue more interest rates; while, the shorter ones will get you out of the well quicker than thought as they have higher installments and the interest rates are not stretched. The benefit of fixed-rate mortgage is that the loan buyer is directed to pay off the same interest throughout the loan term. In this matter, the monthly principal amount and interest payment remains static from the first mortgage payment till the last one. Even if the interest changes in the market, the lender will not change the repayment plans. On the other hand, lowering of interest rates will enable the borrower to secure that lower rate by financing the mortgage again.

The other one is an adjustable-rate mortgage (ARM), which has an interest rate changing according to market fluctuations. But, initially, the interest rate remains fixed for some time period. Initially, the interest rate is kept below the market rate, which makes a mortgage more reasonable in the short term; but not in the long term. There are chances of the interest rate to be increased or decreased later, for which you should be prepared.

Also Read: How Much Can I Afford To Borrow On A Mortgage?

Eligibility for Mortgages:

Indeed, the 1st time home buyer programs indicate that anyone having the ability to keep collateral of good amount and tendency to pay off on time, can apply for the mortgage loans. In case, the buyer stops or is unable to pay the loan; then, the collateral will be used as a mode or repayment and the buyer will no longer have any rights on the collateral kept.

With the help of information mentioned above, Mountview Financial Solutions, a mortgage broker near me in London & Essex will be assisting you in documentation work. They will be helping the buyers to understand the process in detail; so that no confusion is left after, for sure.